Rotterdam 2025 — Storage Capacity, the Energy Transition, and What It Means for Independent Operators

Rotterdam’s tank storage market is navigating a structural transformation — as biofuels, hydrogen, and ammonia gradually enter the terminal landscape alongside traditional petroleum products, independent operators face both investment decisions and commercial opportunities. Rotterdam’s storage market remains the most liquid independent petroleum storage market in Europe, but operators who invest in product flexibility — multi-product […]

Kazakhstan’s Methane Regulations — What Every Storage Operator Must Do Now

The September 2025 MOU between Kazakhstan’s Ministry of Energy and the Global Methane Hub has introduced satellite-based methane leak detection across the country’s oil and gas infrastructure. Following a 2.8 billion KZT fine imposed on a Kazakhstani operator for a 2024 methane blowout, regulators have made clear that fugitive emissions enforcement is now a priority. […]

IMO 2020 at Five Years — The VLSFO Market from Rotterdam to Fujairah

Five years since the IMO 2020 global sulphur cap came into effect, the VLSFO market has matured considerably — but quality variability, supply chain complexity, and the technical demands of blending compliant fuel remain significant challenges for shipowners and bunker buyers. At our Rotterdam and Fujairah terminals, we have refined our VLSFO blending programme to […]

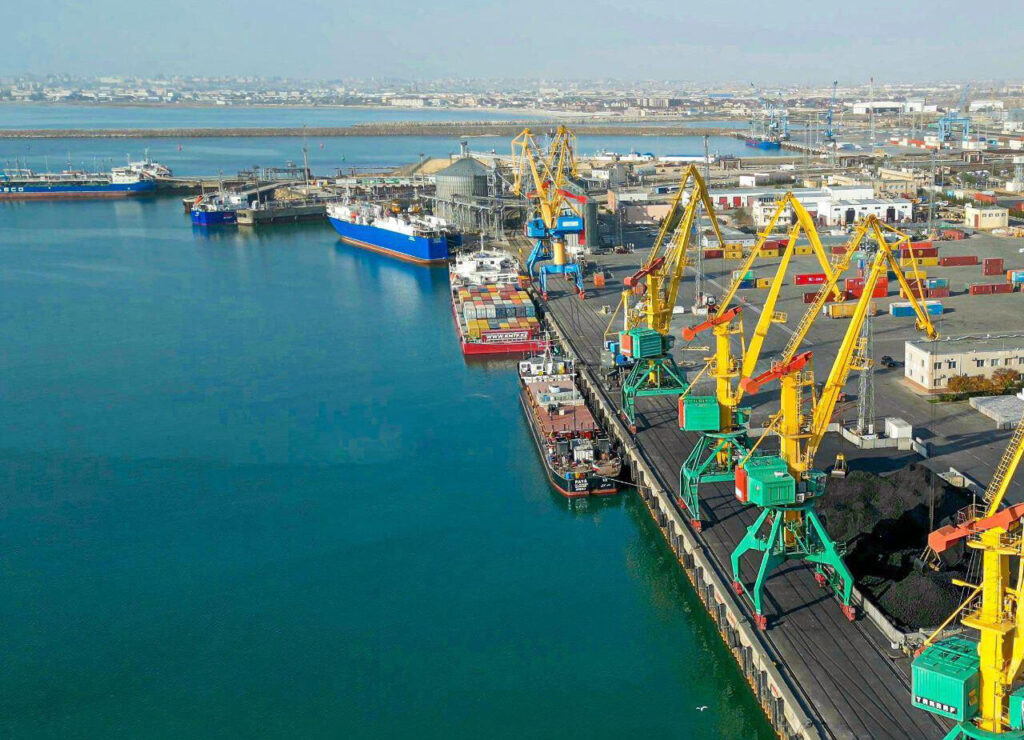

Kazakhstan’s TITR Opportunity — Why the Middle Corridor Is Reshaping Caspian Oil Logistics

As the Trans-Caspian International Transport Route (TITR) gains momentum as the preferred non-Russian export corridor for Kazakhstan’s crude oil, the demand for storage and logistics infrastructure along the route is growing rapidly. Kazakhstan exported approximately 1.8 million barrels per day in 2025, with a growing proportion routing via Aktau and Kuryk through Azerbaijan, Georgia, and […]